What Spain’s State Budget Rejection Means for Non-Lucrative Visa Holders in 2026

If you live in Spain — or are planning to move here — on a non-lucrative visa (NLV), one of the key questions heading into 2026 is whether you’ll need to demonstrate higher savings or passive income.

In short: the latest budget situation in Madrid makes it more likely than not that the financial threshold will remain unchanged.

If you’re still weighing up residency routes, start with our overview of Spain’s visa options and the dedicated hub for Visa Options (Legal & Residency).

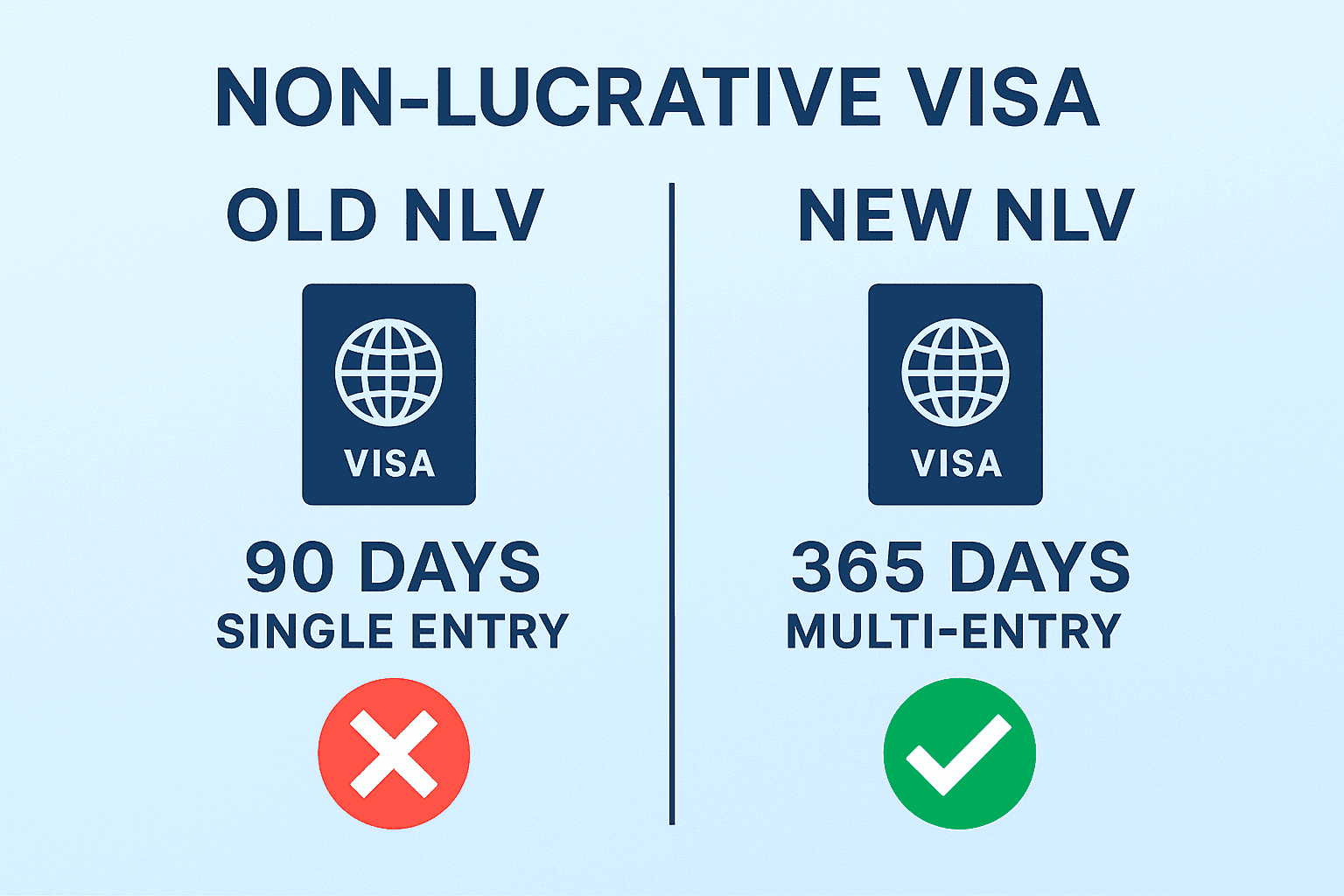

What Is the Non-Lucrative Visa?

The non-lucrative visa is one of the most common ways for non-EU nationals to reside in Spain without working locally. It’s often used by retirees or those with reliable passive income, because the core requirement is to prove you can support yourself (and any dependants) without a Spanish salary.

For a practical, step-by-step explanation of eligibility, documents and typical timelines, see: Non-Lucrative Visa Spain (2025 guide).

If you’re specifically concerned about taxation while living here, you may also find this helpful: Do I have to pay tax in Spain on the non-lucrative visa?

How the Financial Requirement Is Calculated

The minimum savings / passive income required for the NLV is based on Spain’s IPREM (Indicador Público de Renta de Efectos Múltiples). IPREM is a government reference index used across multiple areas (subsidies, grants, legal aid thresholds and more).

In 2025, the IPREM is:

- €600 per month

- €7,200 per year

NLV holders must generally demonstrate:

- 400% of annual IPREM for the main applicant (€28,800)

- +100% of annual IPREM for each dependant (€7,200 per year)

As a simple example, a couple applying together typically needs to show around €36,000 in qualifying savings or passive income for the first year.

For renewal periods (commonly two years), the requirement is generally higher because you must cover a longer timeframe.

If you want a deeper dive into what counts as acceptable proof (bank statements, pensions, investment income and how consulates interpret them), read: Spain visa financial requirements (2025).

For the broader residency admin context (including NIE essentials), see: Residency & NIE essentials

and our standalone guide: NIE number Spain (expats guide).

Why the 2026 Requirement Is Unlikely to Increase

This is the key point: IPREM is updated through Spain’s General State Budget. Without an approved budget, IPREM typically remains frozen at its current level.

Spain is entering 2026 without a newly approved national budget, following another failed attempt in Congress in December 2025.

As a result, it is highly plausible that IPREM — and therefore the NLV financial threshold — stays the same throughout 2026.

Could the Rules Still Change in 2026?

Yes, it’s possible. If a budget is later approved, the government could update IPREM during the year. However, given recent voting dynamics, many observers expect the status quo to continue unless there is a significant political shift.

It’s also worth noting that IPREM has not increased every year since it was created. That’s why the non-lucrative visa threshold often remains stable, unlike the digital nomad visa where financial requirements are tied to salary benchmarks that tend to move more frequently.

If you’re comparing these options, see: Digital Nomad Visa (DNV) in Spain and

Spain digital nomad visa requirements.

What This Means for Non-Lucrative Visa Holders in 2026

Barring an unexpected budget agreement, the practical takeaway is straightforward:

- Most applicants and renewals should expect no increase in the NLV financial threshold during 2026

- IPREM-based requirements are likely to remain aligned with 2025 figures

- Planning is easier, because the goalposts are less likely to move mid-process

Even so, consulate and immigration office interpretations can vary, and documentation standards can be strict.

If you’re preparing a move (or renewal) it helps to have the wider “buyer’s admin” checklist covered too: Buyer’s checklist and the step-by-step Buying process in Spain.